The Hard Costs and the Soft Costs of Your Law Firm

If you are new to law firm accounting or an attorney just starting, you might find it puzzling how to enter any expenses for your clients.

Learning about client costs is where the lingo gets a bit fun. Are they hard costs? Are they soft costs? And how should these be booked into the accounting software?

I've seen multiple methods. Some I agree with, and some that I don't. The best place to start this entire conversation is with the IRS. It's essential to know how the IRS looks at these expenses.

IRS publication 502

(1) Attorneys, particularly those working on a contingency fee basis, may advance costs and other expenses for their clients. Such expenses can include but are not limited to, reproduction costs, court reporting, and stenographic costs, filing fees, travel expenses, and communication costs (i.e., long-distance telephone calls, etc.). These will normally appear in an asset account such as Unbilled Advanced Client Costs (until they are actually billed, of course). The examiner should determine if the reimbursements received from the client have been reflected in taxable income through either inclusion in gross receipts or as an offset to the actual expense

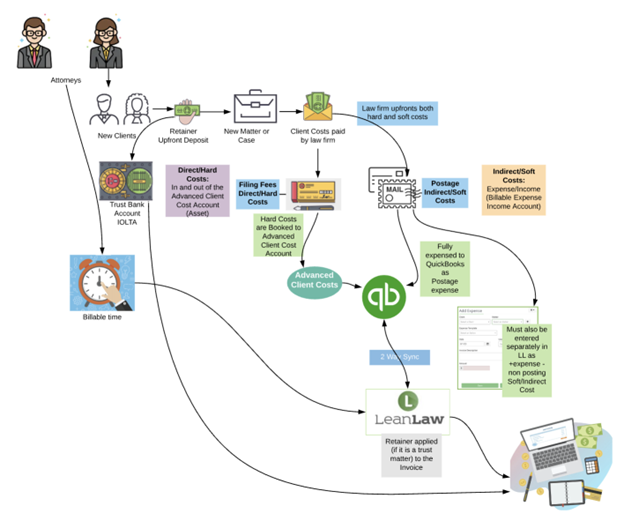

Let's set the stage. The law firm's new client has handed over a retainer or an upfront deposit at the law firm. This deposit is held in a trust bank account. This money is not the law firm's money just yet.

Examples of hard costs:

- Interpreter fees

- Witness fees

- Costs of medical records

- Deposition fees

- Filing fees

- Expert reports

- Photographs

- Laboratory tests

- Sheriff's fees

- Process servers

- Investigators

- Travel expenses

It can be quite an expensive filing fee. For example, a client of the firm's matter has a filing fee paid by the law firm so can bring it into court. Here in Florida, the fee is $450 to file a case in the court system. Who pays for the fee? If it's paid by the law firm operating account, it's an advanced client cost. The law firm has loaned the client this amount of money until it's time to bill the client, and the law firm is reimbursed.

How do you enter these in the accounting software? Do you make a filing fee expense and book the transaction there? In the eyes of the IRS, these fees are an upfront loan by the attorney to the client. You must enter it as such. The transaction would look like this:

Debit: advanced client cost account, which is an asset.

Credit: the operating bank account

If you're using legal technology to process client transactions, you will see this as a work-in-process transaction.

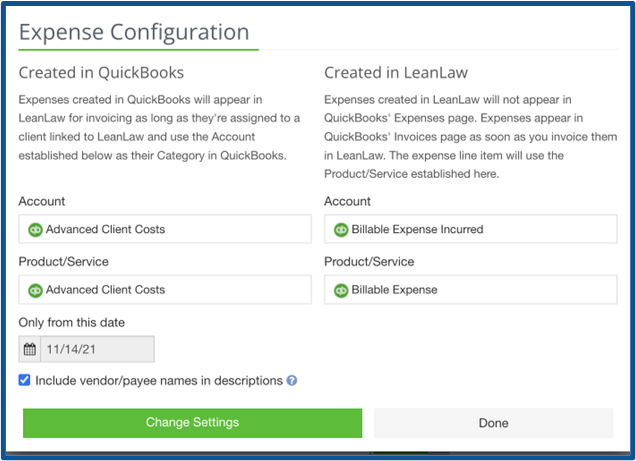

It all comes down to settings, when connecting QuickBooks, for example, to LeanLaw. The setting for advanced client costs is the advanced client cost account, which is an asset account. Yes, it's that simple.

Sweet Automation

We preferred to use Dext as our accounts payable and expense management program. I love that if you're using QuickBooks Online Advanced and Lean Law, this process falls into "the Look Ma, no hands" method.

You have the attorneys each have a user in Dext. Here is where they can have access to the accounts payable holding space. They can snap a picture and upload a receipt in seconds. You can preset many repetitive expenses, like filing fees, as advanced client costs.

Bookkeeping Tip

Don't auto-publish these transactions. If you auto-publish, you must ensure that the client's account is tagged in the transaction. Tagging will vary by each uploaded receipt. Once published, the transaction moves to the system and lands in the advanced client cost account in QuickBooks, where it's read by Leanlaw and ready to be billed back to the client.

Additionally, you can set up any recurring expenses that come into your inbox to go into the inbox for Dext.

Expenses Paid out of Trust

Some state bar associations allow attorneys to pay for client expenses directly from the trust bank account. But what if this expense is paid out of the trust account? How is that entered? You want to ensure that you post this transaction in that sub-matter for that particular client. It will land in that liability account, reducing the amount of money in the retailer that the law firm holds.

Soft Costs

But what about the soft costs? And what the heck are soft costs?

These soft cost expenses are handled at the law firm and are typically "administrative" expenses. For example, this could be a postage expense that the law firm just pulled a stamp or two off of their stamps used at the law firm. Soft costs can also be copying charges that a legal assistant may have to copy some documents and mail them to the client.

How do you book these?

Since there's no way of tracking these small expenses by the client, the best way to book these is to determine the price you will charge for these small expenses upfront. You could say all mailings are going to cost $10 for FedEx.

Some firms charge just a percentage of the entire case or matter as an administrative fee. When using the "administrative fee" method, the attorneys do not have to track the minutiae of soft costs.

The soft cost is entered as firm expenses, which are debited. They are paid for out of the operating account. That's your credit. But when you book these in for the customer, they have to be booked in as billable expense income as the offset when you bill them back to your client.

All client expenses or possible expenses must be communicated to the client before any contract or agreement is set in place. It's critical for a happy client-attorney relationship.

As a bookkeeper, the account for holding advanced client costs must be reconciled monthly. It's imperative to do this because we need to ensure that all the expenses for each client I billed back, or they become law firm expenses.

I hope this article was informative in explaining the bookkeeping transactions around hard and soft costs. We are just a phone call away if you are an attorney and need help with your bookkeeping or accounting needs. Our number is 239-848-0001.

QuickBooks Online for Attorneys

Are you an attorney and want to use QuickBooks for your accounting software but don’t know where to start? Download this free e-book today!

Download E-book

We have a course! Fast Track Legal Accounting!

Are you an accountant or bookkeeper that just landed your first attorney-client and needs to know where to start? Do you have a few but want to serve them better? We have a course to get you started!

Learn More